Excel template mortgage refinance calculator

Excel template mortgage refinance calculator

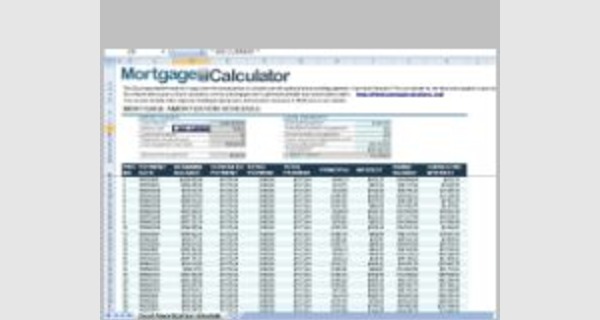

This article provides details of Excel template mortgage refinance calculator that you can download now.

Microsoft Excel software under a Windows environment is required to use this template

These Excel template mortgage refinance calculator work on all versions of Excel since 2007.

Examples of a ready-to-use spreadsheet: Download this table in Excel (.xls) format, and complete it with your specific information.

The development appraisal excel template will allow you to calculate either the land value of a potential development site, or assess the profitability of a project which you are looking at.

To be able to use these models correctly, you must first activate the macros at startup.

The file to download presents four templates Excel template mortgage refinance calculator

- Excel mortgage calculator

This Excel spreadsheet makes it easy to view the amortization of a home loan with optional extra monthly payments.

- Mortgage Refinance Spreadsheet

Instructions

The calculator updates results automatically when you change any input.

- loan amount- the amount borrowed, or the value of the home after your down payment.

- interest rate- the loan's stated APR.

- loan term in years- most fixed-rate home loans across the United States are scheduled to amortize over 30 years. Other common domestic loan periods include 10, 15 & 20 years. Some foreign countries like Canada or the United Kingdom have loans which amortize over 25, 35 or even 40 years.

- payments per year- defaults to 12 to calculate the monthly loan payment which amortizes over the specified period of years. If you would like to pay twice monthly enter 24, or if you would like to pay biweekly enter 26.

- loan start date -the date which loan repayments began, typically a month to the day after the loan was originated.

- optional extra payment - if you want to add an extra amount to each monthly payment then add that amount here & your loan will amortize quicker. If you add an extra payment the calculator will show how many payments you saved off the original loan term and how many years that saved.

Why would anyone want to refinance their home mortgage? The short answer is: “it may make financial sense.” If you hear that interest rates are going down, you may want to consider refinancing your loan. The general rule is: If the new loan results in at least a 1 percent, and preferably a 2 percent decrease in your interest rate, then refinancing may be worth considering.

People refinance their homes to take advantage of lower interest rates or to decrease their monthly payment. Sometimes it is done to create extra money for purchases (like a car) or for debt repayment. This type of “cash-out refinance” adds to the total debt and increases the time and cost of repaying the loan. And if your credit score is low, lenders will consider you a higher credit risk and charge you a higher interest rate. While mortgage payments are often thought of in terms of the “principal” initial amount you’re borrowing, interest payments on the principal can dramatically increase the amount you’re paying in Refinancing may be an important step in your retirement plan. As you think about the age you want to retire and the fact that you will likely have a fixed income at that point, you may want to look into ways to pay off your mortgage before retirement.

Some families inadvertently pay thousands and thousands of dollars beyond what they could have if they had taken the proper time to refinance their loan. On the flip side, while refinancing may seem like a sure bet to save money, there are some major considerations to think through as to whether you will be able to break even on the loan.